5 Ways to Boost Your Mortgage Pre-Approval

Getting pre-approved is a huge first step. It basically gives you a shopping budget so you know exactly what you can afford when you start looking at homes. But sometimes, the number you get back from the bank is lower than you were hoping for, which can really put a damper on your plans.

If your pre-approval came in a bit low, don’t stress. Here are five simple ways to help bump that number up.

1. Tackle Your Monthly Debts

Lenders look at your "debt-to-income ratio." Basically, they want to see how much of your monthly paycheck is already spoken for by things like car payments, credit cards, or student loans. If you can pay down (or pay off) some of those high-interest debts before you apply, it frees up more of your income, which means the lender can offer you a larger mortgage.

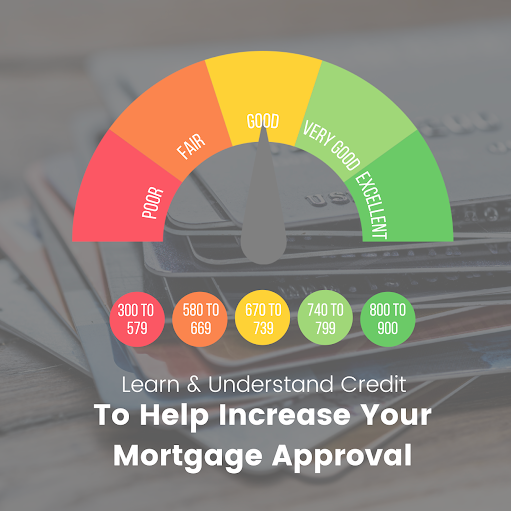

2. Give Your Credit Score a Boost

Your credit score is a big deal to lenders. It’s how they decide how risky it is to lend to you. If your score is on the lower side, you might not qualify for the maximum loan amount. Before you start house hunting, check your credit report. Making sure your bills are paid on time and keeping your credit card balances low can help push your score up and open the door to a higher loan.

3. Play Around with the Mortgage Terms

The type of mortgage you choose actually changes how much you can borrow. Because of the "Stress Test" in Canada, you usually have to prove you can handle a higher interest rate than what you’ll actually pay. Right now, variable rates are often higher than fixed rates, so choosing a fixed rate might actually help you qualify for a bigger loan. We can look at the different options together to see which one gives you the most buying power.

4. Aim for a Bigger Down Payment

The more cash you can put down upfront, the less you have to borrow. This makes lenders more comfortable, and it often allows them to approve a higher total purchase price. If you don't have the extra savings right now, you might consider a "gifted" down payment from a family member or look into government programs designed to help first-time buyers get their foot in the door.

5. Consider a Co-Signer

If you’re still coming up short, you can ask a trusted family member with good credit and a solid income to co-sign with you. Their income gets added to yours in the eyes of the lender, which can seriously increase your approval amount. Just keep in mind that a co-signer is legally responsible for the mortgage payments if you can’t make them, so it’s a big commitment for everyone involved.

Final Thoughts

It’s definitely possible to get a higher pre-approval, but it might take a little time and some planning. Most importantly, make sure you’re comfortable with the higher monthly payments that come with a bigger loan. We always suggest sitting down and looking at your real-life budget—including things like groceries, gas, and utilities—to make sure your new home fits your lifestyle perfectly.

Ready to get started? At COPA, we work with dozens of different lenders to find the best deal for you.

Have questions about your mortgage options? Get in touch - we’d love to help!